Emmanuel Macron, speaking after the Ecological Planning Council on September 25, 2023 to present his vision of a “French-style ecology”, announced that he wanted to “regain control of electricity prices at French and European levels by the end of the year”. This announcement is clearly a response to a strong political expectation in a context of the energy crisis and inflation. The issue is also key for ecological planning based on a massive electrification effort in the building, transport and industry sectors.1 Faced with this dual imperative, this blog post aims to take stock of and analyse the main tools and challenges involved in regaining control in an energy transition context.

- 1According to the 2035 power system outlook published by the French electricity transmission system operator (RTE) ), consumption could rise by up to 165 TWh (+35%) by 2035. This corresponds to an average annual growth rate of 14 TWh, which is higher than that seen during the electrification boom between 1973 and 1990.

Regaining control… does this mean it’s been lost?

Taking back control of electricity implies that control has been lost, which is not entirely evident: France has managed to maintain the regulated electricity price for a large proportion of “small” consumers (households, very small businesses and local authorities), which is demonstrative of (political) control over the electricity price, in the same way as the Regulated Access to Incumbent Nuclear Electricity (ARENH) mechanism provides similar benefits to large industrial consumers and customers of alternative suppliers.2

As a symbol of State price regulation, the “tariff shield”– introduced at the start of the energy crisis in the form of a price freeze on the regulated price, along with the extension of the ARENH to cover a further 20 TWh (120 TWh in total) and the introduction of specific support for businesses and local authorities–has largely absorbed the price shock for consumers, with tariffs rising but staying relatively low compared to European neighbours.

However, the public costs entailed are significant: €28.5 billion in 2023 for electricity, half of which is financed by savings from renewable electricity production (wind power in particular).

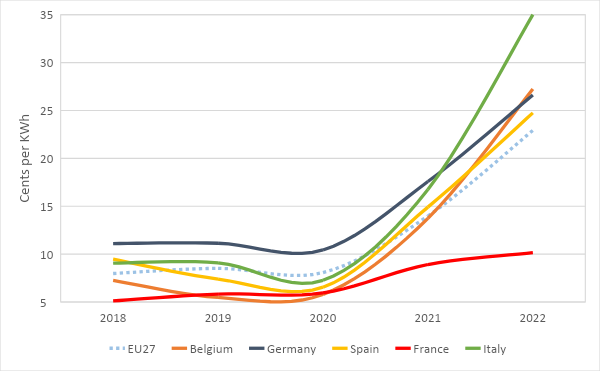

Average electricity price for households, including all taxes (consumption of 2.5 to 5 MWh)

Source: Eurostat data.

Average electricity price for industrial consumers (>150 GWh), including all taxes

Source: Eurostat data

Regaining control also implies agreeing on the reasons for this alleged “loss” of control. From the beginning of the energy crisis, the European electricity market, with its principles of liberalization and pricing based on the marginal cost of the last generating unit used to meet demand, has been the perfect scapegoat.

While the European electricity market reform currently being negotiated is necessary, it should not be forgotten that the impact of the gas crisis on the European electricity market has only exacerbated the weaknesses of the French electricity system observed last year. These include a fall in nuclear production of around one third,3 resulting in a loss of almost €30 billion for EDF, increased reliance on electricity imports and gas-fired power stations, at an estimated cost of more than €20 billion,4 and a number of shortcomings in the ARENH system, which are becoming increasingly apparent.5

Consolidating low-carbon production, the crux of the matter

Considering both the vulnerability of the French electricity system in 2022 and the extremely ambitious political targets for electrification (increase of 10 to 14 TWh annually by 2035), the first conclusion to be drawn is that the development of low-carbon power generation will be the main factor to control electricity prices in the short, medium and long terms.

Pending the commissioning of new nuclear reactors after 2035, this effort must focus on reaching high targets for nuclear power generation from existing reactors (360 TWh in 2030 according to RTE, 400 TWh according to the Minister for Energy Transition) and doubling renewable electricity generation in eight years. This pathway is both ambitious by historical standards, as well as at the lower end of the range of pathways taken by our European neighbours, as illustrated by RTE in its 2023 projected supply estimates. Beyond the divergences that are often highlighted, one can notice that the French target for deploying renewable electricity closely resembles to the trajectory observed for Germany ten years ago, between 2012 and 2020, with an increase from 120 to 240 TWh.

Comparison of targets and development rates (GW per year) for onshore wind, solar PV and offshore wind in France and neighbouring countries (RTE)

Source: RTE 2023 (p.43).

Does regulation mean better control?

The second control lever relates to the regulation of the electricity market. In this respect, the question of what will succeed the ARENH after 2025 takes up a large part of the debate.

However, focusing on the ARENH is often a case of not seeing the wood for the trees: the issue is not so much about EDF selling electricity at a regulated tariff directly or via alternative suppliers, but is more about achieving a “fair price” and the right distribution of low-carbon production, by trying to strike a difficult balance between the divergent interests of: 1) the State as a shareholder and driver of the ecological transition, 2) the operator EDF and its huge investment needs, 3) industrial consumers concerned about their competitiveness, and 4) households.

As shown by the recent disputes between the French government and EDF, and the debates on the cost of producing nuclear power, this issue cannot be resolved through a purely technical approach but instead requires a clear political decision. This need is increasingly understood, as illustrated by the announcements made by the French President and the Minister for Energy Transition. But there should be no rush, given the complexity of the issue and the need for democratic debate. Any proposal for a short-term solution should therefore remain transitional, until a more sustainable approach compatible with the challenges of the medium- and long-term energy transition can be defined.

Renewed regulation raises numerous questions

The “Contracts for Difference” (CFD) scheme, eagerly awaited by France and which forms the heart of the negotiations on the reform of the European electricity market, offers only a partial solution to all of the issues identified at this stage, the devil being in the detail.

- Beyond the general principle of defining a stable price over the long term that benefits both the producer and the various consumers, many practical (and often complex) questions remain unanswered:

- Why regulate nuclear power alone, compared with an approach that would encompass all low-carbon generation (including renewables)? Should we also include a proportionate contribution to the renewal of France’s nuclear fleet (by financing new EPR-2 reactors), at the risk of cementing the dominant position of the incumbent operator?

- Should we set a fixed price or define a price corridor (that sets a maximum and minimum price) indexed to the wholesale market price? Or to inflation? What would be the risks for producers and beneficiaries?

- How should we manage the distribution of contracted electricity to different consumers? Through a system that is equivalent to the ARENH? By selling energy production via long-term purchase contracts? By organizing an ex-post redistribution of revenue from the recovery of inframarginal rents, via a “negative” floating tax on consumer bills?

- Should we aim for the same level of supply prices for all consumers? Or should we accept different price levels depending on needs and priorities, for example by setting a much lower price for electricity-intensive industries, offset by a higher price for households (or vice versa), as has already been implemented for the financing of renewable energies in Germany? Should access to this scheme be conditional on commitments by industrial actors to invest in electrification?

- What are the impacts and interactions with existing wholesale markets, given that between 60% and 90% of French production could end up “under CFD” schemes?7

An urgency to reconnect the French and European debates

Finally, reconnecting the French debate to the European level seems essential, based on a simple but crucial observation: electricity systems are now largely interdependent, and the challenges of electricity market reform are the same in all Member States. How can we strengthen the use of long-term contracts to simultaneously accelerate investment in low-carbon production sources and the electrification of the economy, while giving consumers the benefit of more stable electricity prices and preserving (and ideally optimizing) the operation of existing wholesale markets?

Firstly, this would mean broadening the debate from the outset to consider the relevance of a decarbonized production “pool”, which would be remunerated via long-term contracts, including existing nuclear power generation, nuclear power stations that are in the pipeline, and renewable production, as proposed by European economists such as Michael Grubb and Karsten Neuhoff?

Broadening the debate in this way beyond the sole question of the French mechanism that could succeed ARENH would also make it possible to deal explicitly with the key question of the potential interactions between “transitional” national mechanisms, intended to respond to the effects of the energy crisis, and the advent of a more harmonized European approach by 2030.

This aspect is all the more important given that renewable generation (potentially under long-term contracts) alone is expected to account for up to 70% of the European electricity mix, with low-carbon generation comprising up to 85%. This means that there is a considerable need for flexibility, as well as for good coordination between short and long-term markets.

This also requires us to place the French approach for the ecological transition, which is based on sovereignty and reindustrialization, more firmly in its European context. In particular, regarding the need to rebuild Franco-German cooperation on stronger foundations, based on an objectification of the demands (and fears) on both sides of the Rhine, and the development of pragmatic compromises, in keeping with the EU’s vision of “Union in diversity”.

Agreeing on common principles regarding price levels, volumes and conditions of access to preferential power supply for European industry is therefore a matter of major importance for the EU, to avoid falling into a race to the bottom based on national approaches that are sometimes fragile, with each country trying to protect its national competitiveness through the cheapest prices, while running the risk of jeopardizing Europe’s competitiveness in relation to the rest of the world, in the absence of a collective strategy.

This presupposes, first and foremost, a need to work towards a better mutual understanding of national positions, beyond caricatures and ideological battles. But it also means avoiding the growing pitfall of political narratives framing the question of competitiveness between neighbouring countries, forgetting that the success of the Green Deal will depend on our ability to launch ourselves collectively into the race to develop green industries that can compete with China and the United States.

- 2Regulated tariffs are currently reserved for households and very small professional (or public) consumers. Several bills and amendments have been tabled to extend eligibility for regulated tariffs to local authorities and SMEs, but so far without success.

- 3279 TWh produced in 2022 compared with an average of over 400 TWh over the last ten years.

- 4In 2022, electricity production from gas-fired power stations was marked by a volume effect (+11 TWh for a total of 45 TWh) and a price effect (sharp rise in production costs due to the surge in gas prices and the price of certificates on the EU Emissions Trading System). The difference compared with 2021 can be estimated at up to €15 billion. At the same time, the net trade balance clearly reverses (60 TWh decline compared to 2021), for a net import balance of 16.5 TWh and an estimated differential of €10 billion compared with 2021, according to RTE. (https://analysesetdonnees.rte-france.com/bilan-electrique-echanges#Factureenergetique)

- 5These shortcomings include the failure to adjust the ARENH volume, despite changes in market shares between regulated tariffs and market supplies, resulting in a capping rate and greater exposure to wholesale market prices for all consumers. Another issue has been the unilateral nature of the ARENH (an obligation for EDF, but a “purchase option” for beneficiaries) and the absence of any change in the ARENH price since 2012.

- 760% if the focus is limited to existing nuclear power alone, 90% if all low-carbon generation is included.