The unprecedented energy price rise both in France and across Europe has profoundly upset the political agenda. Coming on top of the current health, social and economic crisis, this new energy “crisis” leads to unprecedented pressure for political decision-makers: how to take urgent action without being over-hasty? How to ensure that measures properly target the most vulnerable? And above all: beyond palliative measures, how to speed up the low carbon transition to better prevent crises in the future?

The scale of the energy price increases depends on the benchmarks selected.

The political debate tends to focus on the evolution of prices in the very short term, taking as a reference point the beginning of the year 2021, or even the historically low levels reached during the global pandemic in May 2020. This distorted perspective helps to give the impression of a truly unprecedented increase, suggesting an even greater scale to this crisis.

Conversely, over a 10-year horizon, the overall increase is much less pronounced, and even shows a significant drop in the price of oil. It is important to note that, for fossil fuels, the recent increases follow a decade-long downward trend in prices. As the main fuel of a world economy dependent on abundant, inexpensive energy, this downward trend has turned into a time bomb.

Evolution of energy prices on wholesale markets and in the European Emissions Trading System (EU ETS)

Natural gas

Oil

Coal

Electricity

EU ETS

May 2020 - Oct. 2021

+1,800 %

+150 %

+400 %

+800 %

+200 %

Jan. 2011 - Oct. 2021

+300 %

-23 %

+100 %

+160 %

+330 %

Price in Oct. 2021

€ 80/MWh

$75/barrel

$240/t.

€140/MWh

€62/t. CO2

In parallel to the rise in energy prices, the price of CO 2 certificates in the EU ETS also hit a record of over € 60 per ton of CO2 in October 2021. However, this increase has only a fairly limited impact on the price increase on the wholesale electricity market: the cost of CO2 represents less than 20% of the marginal production costs of a gas power plant today. It is also regrettable that the ability of the EU ETS to drive a fuel switch between coal and gas power plants is being undermined by the meteoric rise in gas prices.

What is the impact on French consumers?

The real impact of these increases on the bills paid by consumers remains very variable, and depends both on the make-up of the tariffs, the period considered, and household consumption.

For natural gas, the monthly indexation of regulated sales tariffs has led to rapid increases, in line with the evolution of the supply: excluding subscriptions, the increase in the per kWh tariff amounted to 37 % between January 2019 and October 2021, and almost 100 % compared to the record low reached in June 2020. Bill increases may exceed 500 euros over the year for a household using gas for heating.

Evolution of regulated sales tariffs (TRV) for electricity and gas and of the average price of diesel

TRV gas

TRV electricity

Diesel

January 2019 - Oct. 2021

+37 %

+7.4 %

+ 11 %

January 2021 - Oct. 2021

+70 %

+0.5 %

+ 20 %

Price in Oct. 2021

8.73 cents/kWh

15.58 cents/kWh

€ 1.56/l

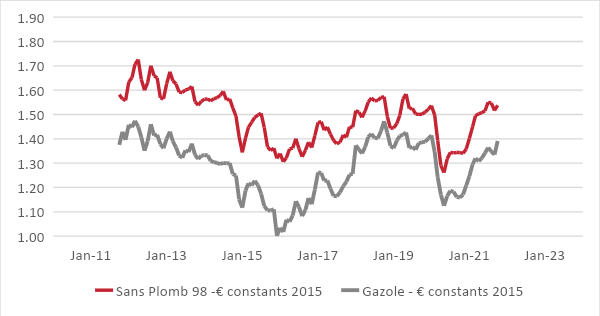

For fuels, a historic “record” was reached in mid-October for the price of diesel (1.56 euros per liter). Over 12 months, the increase was + 27 % for diesel and + 21 % for unleaded petrol 98. However, if we observe the trend over 10 years and take account of inflation, the current price level is similar to that pre-COVID crisis (2019 until February 2020), and lower than the level reached in 2012.

Monthly average price of diesel and unleaded petrol 98 in constant 2015 euros

Source: Iddri, data from MTES (2021) and INSEE (2021)

Finally, for electricity, the impact of the price increase on the wholesale market on tariffs remains very low, due to the relative lack of importance of the market price in the make-up of the regulated tariff and the government decision to limit the increase announced for February 2022 to 4% instead of 12%.

Managing the social aspect of the crisis: key principles to guide public action

The importance of limiting the impact of the current price increase on the most vulnerable is not open to debate. In order to achieve this effectively, it is essential that the measures respond to certain key principles, most of which are echoed in the recent communication from the European Commission on this topic:

- speed of implementation;

- targeting the most vulnerable actors;

- proportionality of the assistance in relation to the real additional cost borne by the most vulnerable actors;

- reversibility and temporary character of the crisis management measures; and

- the public cost of the measures, in view of their effectiveness in taking into account all of these criteria.

Do not confuse urgency and haste: targeting the most vulnerable is an absolute priority

It is obvious that the political measures recently announced in France only respond very partially to the principles mentioned above. The question of targeting remains difficult to address, since it requires the cross-referencing of different data sources (household income, energy for heating, energy performance of housing, limited use of vehicles, etc.). However, it is essential in order to provide an adequate response to households that are most in need, whether it is short-term social assistance or support for the low carbon transition.

However, apart from the additional energy check worth 100 euros, the measures announced (tariff shield, “inflation” allowance of 100 euros) target (almost) all households, with the result that the effect is rather diluted and not proportional to the needs of the most vulnerable, while generating a considerable public cost.

Let us take electricity as an illustration: a public expenditure of 6 billion euros is announced to finance the tariff shield, for an impact of between 30 and 125 euros per household (if the household has electric heating). These same 6 billion euros would have made it possible to finance an energy check of up to 1,000 euros for all of the 5.8 million households who currently benefit from one.

In terms of timescale, one may also wonder whether proposals aimed at reforming energy markets or developing new low-carbon means of production would be able to respond to the difficulties that households and vulnerable people are facing in the very short term.

Financing public action: the issue of redistribution between winners and losers

Another notable fact in the public debate: by focusing (rightly) on the losers of this “crisis,” we forget that it also produces winners, who benefit from very exceptional profits.

For these operators, the stability over time of the tax rules that apply to them is considered essential in order to be able to make long-term investments and convince their investors to support them in such a strategy, which includes counting on moments of exceptional profits as well as less favorable periods. How to ensure that these investment strategies remain credible, while setting up a form of redistribution between winners and losers?

The case of Spain, which has implemented a temporary tax on profits by some electricity producers considered “excessive,” thus gives rise to major controversies between economic operators, government and civil society. However, it has the merit of raising this debate on issues of redistribution, which seems essential from the perspective of a just transition.

Nor should we forget that the French State could also be among the “winners”: the additional VAT revenues linked to the increase in the gas tariff alone could amount to 2 billion euros1 . In addition, dividends received from EDF should also increase sharply. This is revenue that deserves to be earmarked towards measures to help the most vulnerable, as well as those resulting from the increase in the prices of CO2 certificates on the EU ETS.

Preparing for the post-crisis period: the just transition, the mother of all battles

The energy price crisis has pushed low carbon transition policies back to the second rank of priorities. In some cases, it has even led to them being accused of being the cause of these price rises. However, even with colossal expenditure, palliative measures aimed at artificially lowering the cost of energy will fail to limit our vulnerability to future crises, and may even worsen them: low carbon transition policies constitute the only strategy for resilience, beginning with energy efficiency measures.

Accelerating the low carbon transition in a context of pressure on both prices and incomes remains a challenge as vast as it is essential. Yet this crisis has the merit of highlighting the issues and essential principles of a just transition: support for the most vulnerable cannot take the place of transition policies, but must be in synergy with them. In other words: if we are able to mobilize nearly 10 billion euros for palliative actions in the face of rising prices, then the same must be done to help those affected bring about the transition at their level.

This also entails putting back on the table the delicate yet key issue of ecological taxation and the price of carbon. In this regard, the political choice made in recent years not to put the increase in the carbon tax back on the agenda was justified insofar as it was necessary above all to initiate a set of other structural changes (for example those proposed by the 150 measures in the Citizen’s Climate Convention) in order to provide households and individual users with an alternative, and to enhance their ability to switch their own energy consumption. However, the urgency of rapidly implementing climate policies at all scales demands this question be asked very soon, while exploring all the political and financial solutions to the inevitable rise in the price of energy.

As a result of the disruption they produce, crises have the power to bring about a new systemic equilibrium. Let us hope that the upcoming political debates enable us to choose the balance that will prove most resilient to the many challenges that lie ahead.

- 1By considering only the increase in the “supply” side of the regulated gas tariff (from €20/MWh to €80/MWh), additional VAT revenues (at a rate of 20%) amount to €12/MWh, or 2 billion euros if we count the 170 TWh of consumption in the residential sector alone.