At this year’s virtual General Assembly to the UN, Chinese President Xi Jinping pledged that China would peak its emissions ‘before 2030’ and achieve ‘carbon neutrality before 2060’. How should we evaluate this statement? The answer to this question can be thought of in both substantive (how challenging would it be for China to achieve this commitment?) and normative terms (how ‘binding’, understood in the broad sense of the term, is this commitment?)

Achieving a peak and then net zero

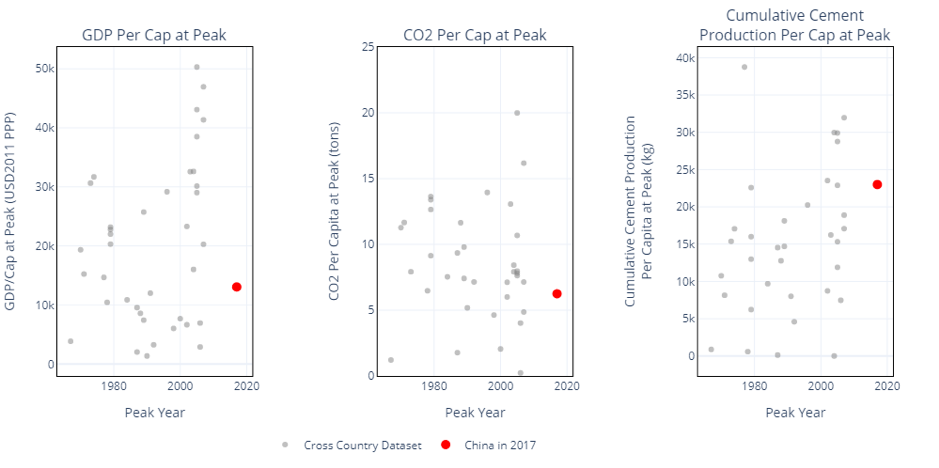

The first component of China’s pledge is to peak its emissions before 2030. We can understand a bit more about the ambition of this component by looking at the experience of other countries who have successfully peaked their emissions. In so doing, we can exclude countries which have peaked their emissions temporarily, or as a result of economic collapse. The figure below gathers a dataset of countries which have: i) peaked their emissions and maintained emissions below the peak for at least 10 years; ii) peaked emissions and grown their economy. The figure displays these countries along several dimensions: CO2 emissions per capita at peak; GDP per capita at peak; cumulative historical cement production per capita at peak. We superimpose on these historical data the position of China in 2017 on each of the metrics listed above.

The figure below deals only in energy-related CO2, which form the largest part of most countries’ GHG emissions, and also of China’s. XI Jinping’s statement also explicitly referred to peaking ‘CO2 emissions before 2030’ and ‘carbon neutrality’, not to GHG emissions or climate neutrality.

In 2017, China’s GDP per capita was estimated at about 13,000 USD2011 PPP; assuming a 5% growth rate, by 2025 it would reach about 20,000 USD2011 PPP. This is well within the range at which a number of Western European countries peaked their emissions: France (22,000), Great Britain (15,000), Germany (20,000). It is also substantially above the range at which former Communist ‘economies in transition’ peaked their emissions, which occurred at GDP per capita levels below where China sits today. These are perhaps better comparison countries for China. For these countries, the transition to a market-based economy unlocked substantial efficiency improvements, allowing them to grow their economies and reduce emissions. Something similar could occur were China to reform its excessively industrialised economic structure. Other developed countries, notably Canada and the USA, peaked their emissions at a substantially higher GDP per capita.

China’s current CO2 emissions are in the order of 6.25 tons per capita as of 2017 and should not grow substantially before the peak is achieved (perhaps up to 7 tons per capita). This level is comparable to or slightly below the level of CO2 emissions per capita in developed European economies at their peak (typically 7-12 tons), but substantially below the level of US and Canada (18-20 tons).

The final metric represents cumulative cement production per capita in the peak year, based on data running back to at least the 1950s for most countries and the 1930s for the developed economies. This metric can be used to understand when emission peaks occurred relative to the build-up of long-lived infrastructure. China’s current level of cumulative cement production per capita is comparable to, indeed higher than, the level at which most countries achieved their CO2 emissions peaks. This is because of the high infrastructure intensity of China’s growth model, and the high cement intensity of its infrastructure.

From the above data, we can conclude:

- China has more or less waited to become a ‘developed country’ before peaking its emissions. However, this conclusion can be nuanced somewhat in several respects.

- China is essentially comparable to developed countries in terms of the extent to which it built up the physical infrastructure underpinning a developed economy before peaking its emissions (seen in cumulative cement production at peak).

- Technology has improved substantially since several Western European (Germany, France, UK) countries peaked their emissions in the 1970s, which explains why China can peak its emissions at a somewhat lower level per capita than these countries achieved.

- China is planning to peak its emissions at a substantially lower level of GDP per capita than achieved by the US and Canada at their peaks, due partly to the very wasteful development model of these countries, and the lower development of the consumer economy in China.

Thus, China’s peak before 2030 appears to be something that should occur ‘naturally’, particularly if China were to reform its skewed economic structure away from emissions-intensive infrastructure. This, however, is not a fait accompli, given the persistent inability of China to lower its investment share of GDP in recent years.

Thus, the real meat of the Chinese announcement is the pledge to reach ‘carbon neutrality’ by 2060. This would entail the complete transformation of the Chinese economy over the course of the coming several decades. Three challenges can be identified here.

Firstly, China’s capital stock is relatively young. In recent years, China has been adding production capacity in high-carbon sectors at a furious pace. This can be seen in the high level of cumulative cement production per capita noted above: the long-term physical foundations of the Chinese economy have essentially been built. Thus, the challenge of reaching carbon neutrality by 2060 is not just one of ensuring that new investments are zero carbon. Achieving carbon neutrality would therefore require China to either scrap a substantial share of economic assets before the end of their economic lifetime, or innovate in terms of technologies to retrofit zero-carbon options onto existing capital stock. Theoretically, this could give a boost to carbon capture and storage technologies, as well as retrofitting of existing blast furnaces, cement kilns, building stock etc. with low-carbon options. At the same time, it seems inescapable that reaching carbon neutrality by 2060 is simply incompatible with a substantial chunk of the capital stock that China has built in recent years. The political economy of retrofits, retirements and asset stranding is thus just as important to China’s zero-carbon pathway as is growth of zero-carbon sources of supply.

This being said, the ramp up of zero-carbon energy sources will have to be dramatic in order to meet China’s energy demand out to 2060, even if this demand grows much slower in the coming decades than it has in the past. Multi petawatt1 scale installations of wind and solar would be required by 2060, implying that China would have to achieve the record-breaking level of wind and solar installation of 2017 every year between now and 2060. Nuclear is also likely to be a part of the zero-carbon supply mix, although its share is likely to be substantially lower than the combined share of wind and solar.

Secondly, although structural change away from investment and towards consumption should naturally reduce demand for products like cement and steel, China is still going to have substantial demand from such so-called ‘hard-to-abate’ sectors. These include heavy industry, heavy freight transport, and aviation. To reach net zero emissions, China will have to innovate net-zero technologies and business models for these sectors, even allowing for some offsetting with negative emissions in other sectors. This will drive forward the decarbonisation agenda outside of the sector of electricity decarbonisation with renewables, and deep into the core of the industrial economy. The hope is that this can drive a second-generation wave of green innovation, similar to that achieved in renewables over the last 15 years.

Thirdly, China’s huge size makes an announcement of a net-zero target potentially transformative at a global level. The spill-overs from a giant country acting strongly on climate will be considerable. Innovation, trade, finance and manufacturing would be transformed. If China goes substantially down this route it will be much harder for other countries to continue to prevaricate; major coal exporters to China, like Australia, are left with deep concerns. At the same time, the substantial innovation that China’s decarbonisation will unleash would facilitate action by others.

Thus, China’s net-zero carbon target is no less challenging than that of the European Union, although the timeframe is extended by another ten years. It amounts to nothing less than the refoundation of a prosperous developed economy on the basis of zero-carbon emissions.

In a nutshell: another Industrial Revolution, this time with the clock ticking.

How binding is the commitment?

This description of the challenge of China’s net-zero pledge naturally raises the question of the normative strength of the pledge. Statements at the UNGA have no legal standing and are not binding in any way. It was already noted above how the statement carefully referenced ‘CO2 emissions’ and ‘carbon neutrality’, leaving some wriggle-room regarding emissions of non-CO2 GHGs.

Nonetheless, the traditional Chinese approach of ‘under-pledge, over-achieve’ suggests that this pledge was not given lightly at all. China has long resisted pressures to enhancing its previous commitment to peak CO2 emissions ‘by 2030’ and has never before given any public indication of its commitments on the mid-century timeframe. A lot will depend on whether China formalises its new pledge in an enhanced ‘nationally-determined contribution’ (NDC), the legally-binding commitments under the Paris Agreement. Here again, China has given indications that it intends to enhance its NDC, although it will probably await the results of the US election in November to do so. The Paris Agreement was deliberately designed to allow the periodic update of countries’ NDCs, and China doing so would give a substantial boost to efforts to corral more countries into doing so. The important litmus test will be how China acts in the near term, both with respect to enhancing its NDC, ensuring that post-COVID stimulus is ‘green’, and opening up the Belt and Road Initiative to more transparency regarding the climate impacts of its investments.

But the true future of China’s pledge likely will be determined outside these legal niceties under the United Nations Framework Convention on Climate Change (UNFCCC), the parent convention of the Paris Agreement. Rather, the key variables for China’s zero-carbon transition lie firmly in the realm of geopolitics. China’s pledge comes at a time when its relationships with much of the world are under intense pressure. China’s regional actions in the South China Sea, Hong Kong, the India-China border, and its internal crackdown on dissent are part of a pattern of a more aggressive, and yet apparently insecure, global power. Meanwhile, the US is riven by internal divisions and deep political disfunction, and both sides of the US political divide have taken a stronger stance against China. Part of this is scapegoating and distraction from the US’s internal, self-inflicted weaknesses. But it also represents concern that the US is now locked in great power conflict with a fundamentally inimical political system.

The more this path of confrontation is trodden, the more insecure China will feel. As we have seen in recent years with Trump’s trade war, the all-important domestic reform of China’s imbalanced economic system will take a backseat in uncertain times as the Chinese government looks to preserve economic and social stability. At the same time, in uncertain times domestic sources of energy like coal are seen as a guarantor of energy security. The more China is split off into a competing block within a fragmented world system of information, trade and finance, the weaker will be the potential innovation spill-overs from China’s decarbonisation pathway.

Thus, we are left after China’s dramatic announcement at the start of a long and uncertain road. Many technologies of a zero-carbon economy remain to be proven. Managing China’s rise is, alongside climate change, one of the pre-eminent challenges of the 21st century. XI Jinping’s statement has set the path. Walking it will take two scarce commodities: innovation and wisdom.

- 1One petawatt is 1,000 terawatts.