The agricultural world is going through a profound crisis, triggered in particular by a feeling of too many constraints and environmental standards, which is rooted in structural problems of income and recognition. The organic sector has not escaped the crisis: having grown steadily since 2010, from 2021 onwards it has been experiencing a gradual decline in France in terms of both value and volume. The main reason for this reduction is said to be falling demand due to various socio-economic factors (loss of confidence, rising prices, insufficient supply, etc.). For this reason the government has chosen to act on organic demand in two ways: by developing certain outlets, and by better informing consumers. This response ignores other dimensions that are central to fine-tuning the analysis and proposing solutions to the crisis. Based on the concept of food environments, this blog post suggests a number of points to consider along these lines, which will be useful more broadly for implementing the agroecological transition.

The “citizen-consumer hybrid”: a concept at the foundation of public policy which shows its limitations in the organic sector crisis

The organic market boomed in 2010, rising from €3.7 billion to €13.2 billion by 20201 . This sustained rise reversed from 2021 onwards, with a 1.3% fall in value. The decline accelerated in 2022 (a 4.6% drop in value terms)2 , and continued in the first half of 2023, when the organic share of food sales fell by 2.7% in value, and by around 10% in volume3 . How can we understand this crisis? In 2022, the Cour des Comptes (French Court of Auditors) published a report analysing support for organic farming and food, and concluded that it was inadequate. On the demand side, the Court highlighted a number of weaknesses in public action: a lack of clarity on labels; competition from labels with less stringent specifications; insufficient communication on health and environmental benefits; and a lack of support and monitoring regarding the 20% target for supplying organic food to public catering.

This mainstream interpretation of the organic sector’s problems is based on a partly erroneous assumption (IDDRI, 2023): namely, citizen-consumers (or “consumer activists”) will make more sustainable purchases if they are shown the benefits of such consumption. With this in mind, the government needs to raise consumer awareness through education (in this respect, public catering is seen as a new outlet for organic food, as well as a lever for education) and information (communication campaigns, nutritional and environmental promotion, labelling) to help people make the “right” choices. At the same time, public authority initiatives aimed at changing the supply side of the market are more subtle: they are mostly voluntary, vague and underfunded, or have very specific impacts on supply outlets that do not account for the majority of sales (canteens, food aid, health establishments, etc.). Public authorities are therefore relying on both the farming sector and consumers to bring about the transition, without however aligning the whole of the agri-food system, despite its structural nature, with the same objectives.

The current crisis in the organic sector shows the limits of the policy implemented since 2010 with the first National Food Programme, and extended in sectoral plans (such as the Ambition Bio 2022 plan), which have failed to embed organic food consumption into everyday life.

Inflation and falling confidence: legitimate but partial explanations

The “inflation” factor is the most frequently cited in analyses of the organic sector crisis. According to this theory, rising prices (particularly food prices) has led households to cut back on spending on products where cheaper alternatives are available, such as branded products, and products with a premium label. This “move downmarket”, coupled with a fall in volume purchases, is having an impact on organic produce.

Added to this is the decline in “confidence” in the organic label and the lack of information. At the same time, the proliferation of products with clear promises (“pesticide-free”, “local”, etc.) with more accessible price positioning seems to be diverting consumer attention4 .

These explanations are backed up by consumer statements: the price issue is the most often cited reason to explain the reduction in organic consumption, followed by a preference for other products (seasonal, local) and a lack of confidence in the label. However, awareness of environmental and health issues, such as the desire to find more organic products in shops or to consume more of them5 , is not in decline.

Rebooting the system: a first step towards a far-reaching change in public action, aiming for efficiency and fairness

In addition to the two cyclical factors (prices and lack of information/confidence), supermarkets are reducing their ranges of organic products (10.7% decline recorded in August 2023 over the course of a year).6 Other reasons, structural in nature, are also having an impact, including: the price differential compared to conventional products; distributor profits and/or the absence of transparency on organic pricing by distributors and food producers; the lack of organic products in certain sales channels (restaurants); the absence of sufficient economic resources for certain social groups; the need to change the way people perceive organic food, etc.7 It is the economic (e.g. price), physical (e.g. shelf space), socio-cultural (e.g. image) and cognitive (e.g. confidence) dimensions that combine to make up “food environments”, which influence organic purchases and, in this case, have not allowed purchasing practices to evolve in a lasting way.

Moving from a “citizen-consumer” approach to one based on “food environments” enables a more detailed understanding of the problems facing the organic sector (Figure 1). The dissemination of this scientific approach, which breaks down the factors influencing consumption practices into four dimensions, is relevant for public action (IDDRI, 2023): it offers a practical and useful system, as an alternative to the consumer-activist paradigm, on which to base action, by allowing the better consideration of factors that actually determine purchasing practices.

Today, the government’s response focuses on inflation and the lack of information, but things are evolving. Statements in 2023 demonstrate the importance of the consumer-activist approach (€3.5m being made available for two communication campaigns), while an announcement has been made on a move towards the more comprehensive consideration of the issues at stake: a “call for transparency” on the subject of supermarket profits; mobilisation of the EU’s “School Fruit and Vegetable Scheme”8 . In the same way, the recommendations of the Cour des Comptes focus on the means of “better informing the choices of citizens and consumers”, while also providing innovative ideas such as calling for supermarkets to introduce transparency on their profits, and proposing a framework for organic product pricing–a subject which the Senate also highlighted in a 2020 report.

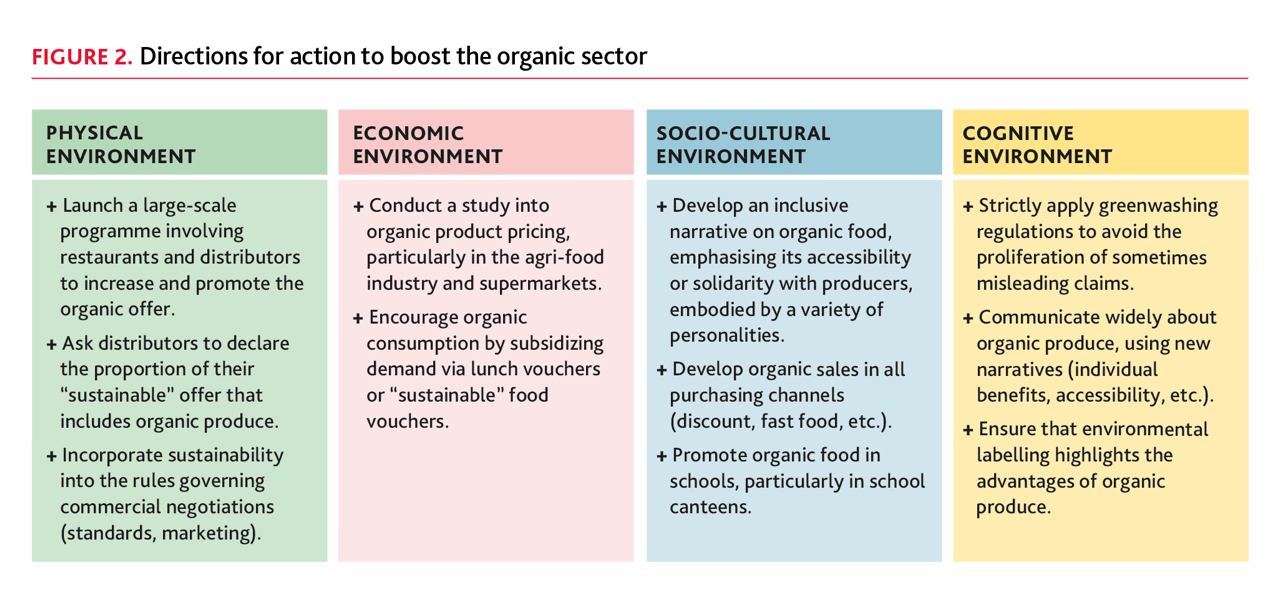

It is now important to confirm this change of direction and to significantly strengthen public action in the food sector. We have made some proposals to this end (IDDRI, 2023), and in Figure 2 we describe some specific ways forward for the organic sector.

Finally, taking action on the food environment in conjunction with food-related concerns and the agricultural transition could provide a response to two frustrations being expressed during the current food and agricultural crisis. The first is articulated by consumers, who are unable to access certain types of food; and the second comes from the farming community, for whom the high expectations (particularly environmental) being placed upon them do not translate into the assurance of selling their production in the absence of sufficient outlets for quality products.

- 1Agence Bio https://www.ecologie.gouv.fr/sites/default/files/Dossier%20de%20presse%20Agence%20BIO%20chiffres%202020-DEF.pdf

- 2Agence Bio https://www.agencebio.org/vos-outils/les-chiffres-cles/observatoire-de-la-consommation-bio/

- 3Renault, C., Chever, T., Lepeule, C., Romieu, V., & Ollié, B. (2023). Evolution des ventes alimentaires biologiques au 1er semestre 2023. Agence Bio, AND International. https://www.agencebio.org/wp-content/uploads/2023/10/Evaluation-marche%CC%81-1er-semestre-2023-Agence-BIO.pdf

- 4See, for example, the article (https://www.lsa-conso.fr/etude-la-consommation-de-produits-bio-marque-le-pas,420996) and (https://www.lsa-conso.fr/le-local-a-la-cote-chez-les-consommateurs-francais-lsa-data,422746) on the appeal of local produce, or the Agence Bio press pack, which states that 73% of the organic sector’s losses in terms of value go to "other labelled products". (https://www.agencebio.org/wp-content/uploads/2023/06/DOSSIER-DE-PRESSE-CHIFFRES-BIO.pdf).

- 5In an OpinionWay/Calif survey conducted in February 2023, in answer to the question "What would you like to eat tomorrow...?" 89% of respondents said they would like to eat "more natural foods" (seasonal, local, unprocessed), 61% said "more organic produce", and 49% "more flexitarian: i.e. greatly reducing animal product consumption, particularly meat". (https://www.calif-solutions.com/barometre-opinionway-pour-calif-les-francais-lagriculture-et-lalimentation/).

- 6LSA : https://www.lsa-conso.fr/bio-reconsiderer-l-offre-et-son-implantation,449456

- 7See for example FNH (2024): https://www.fnh.org/comment-sauver-agriculture-bio/; Gorge, S. “Le bio en baisse : simple ralentissement, ou véritable décrochage” Terra Nova, 15 February 2023 (https://tnova.fr/ecologie/transition-energetique/le-bio-en-baisse-simple-ralentissement-ou-veritable-decrochage/); SYNABIO “Tribune : l’inflation ne doit pas éclipser la transition alimentaire” 15 January 2024 (https://www.synabio.com/tribune-linflation-ne-doit-pas-eclipser-la-transition-alimentaire/); Boutaud, A. and Grimonpont, A. “Une stagnation de la bio ?” (two parts), September 2023, Millénaire 3 (https://www.millenaire3.com/ressources/2023/une-stagnation-de-la-bio-1-2-decryptage-des-chiffres-et-tendances).

- 8Plein Champ, 17 May 2023 (https://www.pleinchamp.com/actualite/un-plan-de-soutien-de-pres-de-200-millions-d-euros-a-l-agriculture-biologique); Terre-net, 30 November 2023 (https://www.terre-net.fr/ministere-de-l-agriculture/article/859255/l-enveloppe-de-soutien-au-bio-passe-de-60-m-a-94-m).